FINANCIAL PROTECTION:

ENSURING A SECURE FUTURE FOR YOU AND YOUR LOVED ONES

ENSURING A SECURE FUTURE FOR YOU AND YOUR LOVED ONES

Welcome to our July/August 2024 Newsletter.

Nobody wants to consider what would happen if they became too ill to support their family financially. Financial protection is essential to creating a secure future for your loved ones, but understanding what cover you may need can be confusing.

On page 8, we discuss whether you have considered the implications financially if you or someone in your family were unable to earn money, became ill or were to die prematurely. It’s not something we like to think about, but if you have left regular employment and are now either retired or have become self-employed, then any previous protection you received from an employer becomes your responsibility.

On page 05, we delve into a new analysis of FCA figures. Since 2015, individuals over the age of 55 with defined contribution (DC) pension pots have enjoyed full freedom to decide how to manage their pensions; purchasing an annuity (a guaranteed income for life) is no longer mandatory. We examine how people have utilised these newfound freedoms and the tax implications that have followed.

On page 10, we look at ways to potentially reduce a Capital Gains Tax (CGT) liability. Cuts to the CGT exemption mean that arranging your investments as tax-efficiently as possible is more important than ever.

Trusts are a powerful tool for estate planning, providing flexibility and control over asset distribution. Properly structured, they can address various scenarios and requirements, ensuring that your legacy is managed according to your wishes long into the future. Read the full article on page 06.

A complete list of the articles featured in this issue appears on pages 02

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

PRE END OF YEAR TAX PLANNING

Welcome to our latest issue.

As we approach the end of the current tax year on 5 April 2024, it’s an opportune moment to examine both your personal and business finances to ensure they are structured to optimise your tax efficiency. Despite the ongoing freeze on many tax rates and thresholds, numerous strategies remain for efficiently organising your financial matters,

Investment scams are a rising concern, promising potential investors the allure of making a significant amount of money swiftly and effortlessly. These scams often involve minimal to no risk investments in various areas such as financial markets, property, cryptocurrencies and precious metals and coins.

A complete list of the articles featured in this issue appears on pages 02 and 03.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Financial Planning In Your 50s: A CRUCIAL DECADE

As we approach the end of the year, taxpayers should begin assessing their tax obligations.

By understanding your tax obligations early on, you could avoid unwelcome surprises (see Page 5).

We also consider Timing the Market (see Page 10), strategies to minimise Retirement Tax (see Page 6), and to create Positive Impact on Financial Wellbeing (see Page 19).

For a full list of contents, please see Page 3.

If you are sailing into your 50s, it becomes pivotal to consider your financial strategy. We understand that knowing where to begin can be daunting, whether you are aiming to maximise your earnings or lay down a robust financial plan (see Page 9).

With our guidance, you can develop and adapt a strategy designed to help you achieve your financial objectives.

Our role is to remove the effort from managing wealth, allowing you and your family to enjoy it instead.

Do not hesitate to contact us for more information about how we can help you visualise your financial future.

EARLY GIFTING OF PART OF YOUR INHERITANCE

TO A FAMILY MEMBER

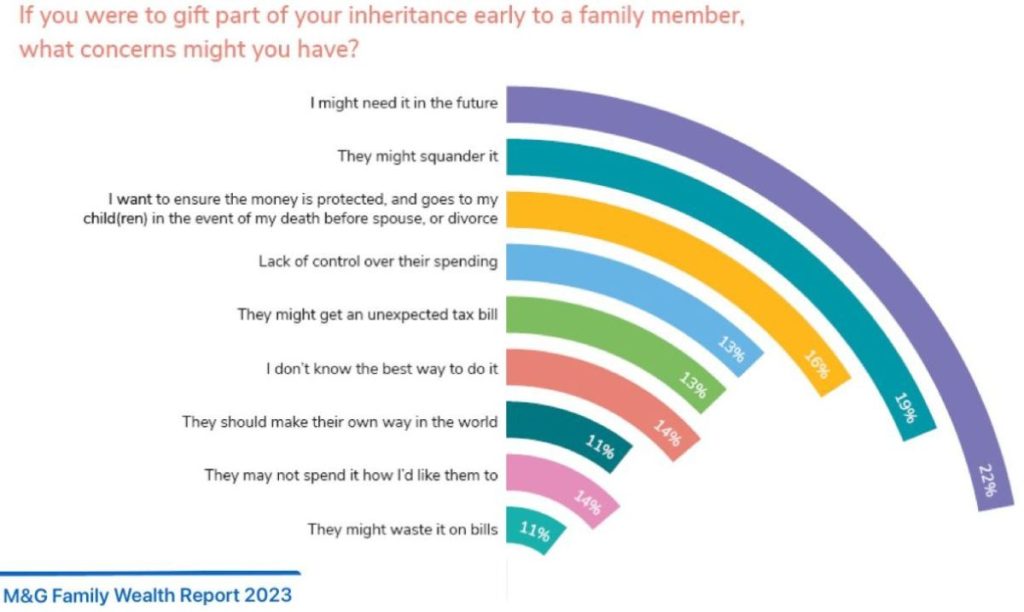

If you were to gift part of your inheritance early to a family member what concerns might you have? An estimated £5.5 trillion will be passed between generations over the next 30 years and the biggest concerns that come up are illustrated below For those looking for a bit more control and flexibility, let’s chat about how we can help

GETTING RETIREMENT READY

Key Steps to Achieving a Comfortable Retirement

Although retirement may appear distant at the moment, there’s much to consider. Let us assist you in navigating this crucial life milestone.

We also cover 10 Reasons to get your Tax Return Filed now.

Our comprehensive financial planning services are designed to align with your current and future goals.

GUIDE TO WEALTH SUCCESSION:

PENSIONS OF SIGNIFICANT VALUE

Welcome but unexpected changes to Pension Tax

The Budget in March brought some welcome but unexpected changes to pension tax, the most significant of which was the abolition of the pension Lifetime Allowance (LTA) charge. You could now expect significant changes that will affect your retirement savings. On page 10 we consider how these changes could impact you.

As we are already in the new tax year you may wish to consider using Investment Allowances to ensure that your money is protected from taxes and also benefits from having more time to grow. This can result in a bigger savings pot in the long run. Read the full article on page 06.

GUIDE TO WEALTH SUCCESSION |

SPRING BUDGET STATEMENT 2023

Analysis of the key tax changes and outlining the practical implications for you, your family and your business

One of the most interesting announcements for our clients included the abolishing of the Lifetime Allowance on tax-free pension contributions, which was previously set at £1,073,100. This is good news for higher earners and those with large pension pots. The standard tax-free annual pension contribution amount will increase from £40,000 to £60,000 from 6th April 2023.

Changes take effect from the new tax year starting 6th April 2023 and we will be happy to discuss the implications and benefits for you.

GUIDE TO WEALTH SUCCESSION

MAKING THE RIGHT PREPARATIONS FOR FUTURE GENERATIONS

In this issue, financial planning can be an uncomfortable conversation for many, but thankfully attitudes towards talking about money are changing. Wealth succession should be an integral part of your financial plan as early as possible – because the right preparation now can have positive long-term impacts on future generations.

On page 06, before you start this process, we consider the questions you need to ask.

GUIDE TO REVISITING YOUR FINANCIAL PLAN IN 2023

Here's our useful guide to revisiting your financial plan in 2023

SHOW ME THE MONEY

HOW TO INVEST YOUR MONEY AND AVOID COSTLY MISTAKES

It’s not surprising that the world of investing can seem complex, especially in the current global economic climate. Investors face an endless supply of market news, many investment choices and often-changing market conditions. There are a number of key principles that every investor should follow with the aim of building an effective long-term strategy designed to achieve their financial goals.

On page 6 we look at ten principles that every investor needs to know. A full list of articles featured in this issue appears on Page 2.